Latest articles on Life Insurance, Non-life Insurance, Mutual Funds, Bonds, Small Saving Schemes and Personal Finance to help you make well-informed money decisions.

Taking adequate insurance to cover your trip as well as stay throughout the academic year is important.

With the US, UK and Canada opening up to Indian students who have secured admissions in their universities, many are gearing up to fly out to their campuses in August.

Last year, many had to defer their admissions by a year due to the COVID-19 pandemic. But this year, the rollout of vaccines has made their journey possible.

If you are amongst them, July is bound to be a hectic month for you, with getting vaccinated, securing Visas and readying other documentation being on top of your mind. However, the scramble to reach your campuses should not make you overlook taking adequate insurance to cover your trip as well as stay throughout the academic year.

Why get insured?

For one, your university is likely to insist that you must have a cover. If you do not obtain one before you fly out, you will have to sign up for the institution-facilitated medical cover as part of your course fee.

Even if the university does not mandate a cover, you will stand to benefit if you buy one. Your regular health cover will not come to your aid if you fall sick during your stay abroad. Unlike business or leisure travellers, you will spend more time overseas, and are likely to need medical treatment at some point in time. In these pandemic times, the risks have only increased. The cost of healthcare in countries such as the US, for example, is exorbitant and could wipe away your family’s savings if you have to be hospitalised for COVID-19 or other illnesses.

In addition, student travel policies, unlike regular international travel covers, pay for other expenses too. For example, missed flight connection, loss of baggage or passport. In case of unfortunate demise of the sponsors – parents or others – who fund insured students’ course fee, the insurer will pay the balance fee to the extent of the sum insured. These policies also pay for return flight tickets of your parents if they have to pay a visit during your hospitalisation.

University vs Indian insurance covers

Buying overseas student covers before you leave Indian shores seems like a good idea, but there are some caveats you need to bear in mind. “Some universities in the US that have tied up with US-based insurers do not accept Indian insurance covers. This is one of the reasons why the pick-up is muted in this category. We hope more universities accept Indian insurance covers this year,” says a senior insurance industry official who did not wished to be named.

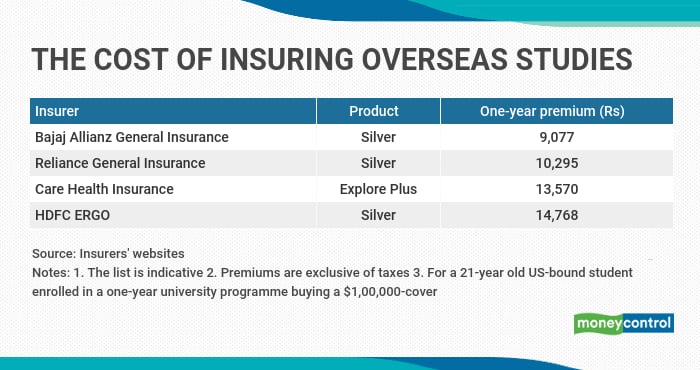

If your independent cover does not meet the requirements laid down by the university, you could face a catch-22 situation. Therefore, ensure that your independent cover ticks all the boxes. If you obtain a cover from an Indian insurer that is acceptable to your university, you stand to make significant savings on your premium outgo. “Indian policies are significantly cheaper than the ones facilitated by universities abroad. So, you must go through the university policy’s features first and look for an equivalent from an Indian insurer,” advises Nikhil Apte, Chief Product Officer, Health Insurance, Royal Sundaram General Insurance.

Also, premiums of insurance covers facilitated by universities have risen over the last one year due to COVID-19, say education consultants. On the other hand, Indian insurers’ travel premiums have remained unchanged. “The premiums have not gone up compared to last year’s rates as the travel insurance portfolio did not see a steep rise in claims last year, with people preferring to avoid travel during the period,” says the official quoted earlier.

If your university insists on its pre-set plan, you can try to convince the authorities about your cover’s adequacy. “Even if your university has a mandatory policy, you could enquire whether you can buy an alternative, equivalent policy. You might have to submit a form or confirmation of coverage documents to show that you have adequate student health insurance,” explains Apte.

However, some education consultants recommend university-facilitated policies over Indian overseas student insurance covers. “The terms of coverage are better as these policies are designed by local insurers in consultation with the universities. These fulfill all the requirements that universities specify,” says Rohan Ganeriwala, Co-founder and Director, Collegify, an education consultancy firm.

Keep an eye on exclusions

While a student cover does offer financial security, you need to be aware of expenses it will not pay for too, particularly in the context of COVID-19. “UK Universities are covering the quarantine costs (mandatory on arrival) for incoming international students. In other countries, the student has to bear the quarantine costs,” says Ganeriwala. While some universities offer quarantine facilities at the dorms on their campuses, some have tie-up with hotels for the purpose.

“In most countries, the vaccination is free. However, if there are costs involved, overseas student policies can cover it as part of outpatient department (OPD) expenses. Mandatory isolation on arrival is not covered,” says Apte. Then, there are claims that are simply not payable – such as legal expenses arising out of students engaging in illegal activities or violating the law or resisting the law.

These policies also come with deductibles – that is, you have to make an initial payment before the policy coverage is triggered. You might have to pay the first $30-50 out of your pocket before the insurer steps in to meet the balance expenses. Be aware of the sub-limits too. Your policy, for instance, could impose a cap of $1,500-10,000 on compassionate visit expenses.

Follow us on our social media channels:

Copyright © 2025 Design and developed by Fintso. All Rights Reserved

Industry News

Industry News